If you’re a Bronx homeowner facing foreclosure, HPD violations, probate, a difficult tenant, or a property in distressed condition, this resource was built for you. 718Homebuyers has compiled answers to the 49 most important questions Bronx families ask before making a decision about their property, with straight answers and no sales pressure.

This guide is educational — if you decide you want help, you’ll see simple next steps below.

Use the table of contents to jump to the section that matches what you’re dealing with right now.

- Foreclosure & Pre-Foreclosure In New York State

- HPD Violations & Code Enforcement

- Probate & Inherited Properties

- Selling As-Is & Distressed Properties

- The Cash Buying Process

- Tenant-Occupied Properties

- Bronx Market & Legal Context

- What Can You Do Now?

Last updated: March 2026

Keith Morris — 718Homebuyers (Bronx cash home buyer since 2013)

Specialties: foreclosure, HPD violations, probate, tenants

718-503-2233 • Keith@718homebuyers.com • 718homebuyers.com

Note: This guide is general information, not legal or tax advice. For your situation, speak with a New York attorney and/or CPA.

Foreclosure & Pre-Foreclosure In New York State

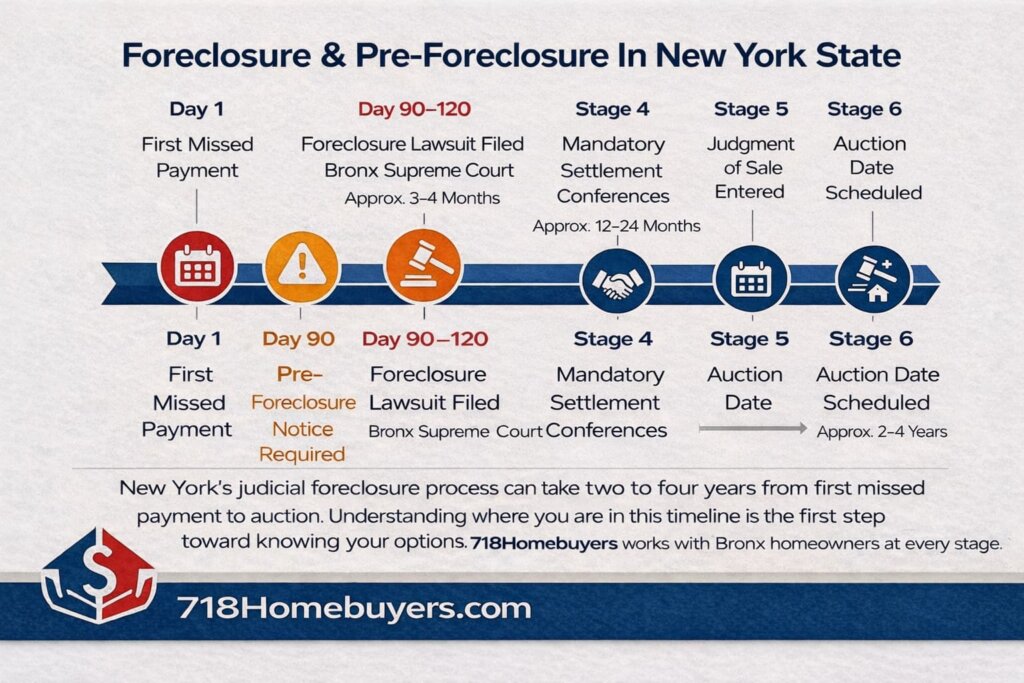

What is the foreclosure process in New York and how long does it actually take in the Bronx?

New York is a judicial foreclosure state, which means your lender can’t just take your home — they have to sue you in court first. That process runs through the Bronx Supreme Court and historically has been one of the longest foreclosure timelines in the entire country. From the first missed payment to an actual auction date, the process can take anywhere from two to four years depending on how backed up the courts are and whether you respond to the lawsuit.

Here’s what that timeline generally looks like: after 90 days of missed payments your lender is legally allowed to file a foreclosure action. They serve you with a summons and complaint, you have the right to respond, and the case enters the court system. From there it moves through mandatory settlement conferences, motion practice, and eventually a judgment of foreclosure and sale before your home can be auctioned.

The length of this process is both a curse and an opportunity. It’s a curse because the debt, interest, and fees keep growing the entire time. It’s an opportunity because it gives you time to make a decision on your own terms rather than having one forced on you. 718Homebuyers has worked with Bronx families at every stage of this process — some who called us the day they got served, and some who called us two weeks before an auction date. Either way, options exist and we’ll help you understand every one of them.

As of early 2026, the average foreclosure timeline in the Bronx remains approximately 650 to 900 days, though post-2025 administrative shifts in the NYC court system have aimed to reduce the backlog of roughly 12,000 pending cases across the five boroughs.

Source: NYS Unified Court System — Foreclosure Statistics.

I just missed my first mortgage payment. Am I already in foreclosure?

No — and this is one of the most common fears we hear from homeowners who call us. Missing one payment does not put you in foreclosure. It puts you in default, which is a different thing entirely.

Foreclosure is a legal process that requires your lender to file a lawsuit against you in Bronx Supreme Court. That doesn’t happen after one missed payment, or even two. Most lenders won’t initiate foreclosure proceedings until you are at least 90 to 120 days behind, and many wait considerably longer before filing — especially in New York where the court process is expensive and slow for them too.

What happens in those early months matters though. Your lender will begin reporting the missed payments to credit bureaus, late fees will start stacking, and you’ll begin receiving collection calls and written notices. Around the 90-day mark you should receive a formal 90-day pre-foreclosure notice, which is required by New York State law before any foreclosure action can be filed.

That notice is your signal to start exploring your options seriously. If you’ve received one and you’re not sure what to do next, that’s exactly the kind of situation 718Homebuyers helps Bronx families think through every week — no pressure, no obligation, just a straight conversation about what’s possible and what makes sense for your specific situation.

Under RPAPL § 1304, the 90-day pre-foreclosure notice remains a strict condition precedent for filing; 2025 legislative sessions reinforced that failure to strictly comply with mailing and language requirements results in the immediate dismissal of the foreclosure action.

Source: NYS Senate — RPAPL § 1304

What is a pre-foreclosure notice in New York and what do I do when I receive one?

A pre-foreclosure notice — sometimes called a 90-day notice — is a formal written notice your mortgage servicer is required by New York State law to send you before they can file a foreclosure lawsuit. It’s not the lawsuit itself. It’s the warning that one is coming if things don’t change.

The notice has to include specific information: the amount you owe, a list of government-approved housing counseling agencies, and a statement of your rights. New York has some of the strongest homeowner protection laws in the country and this notice requirement is part of that framework.

When you receive one, here’s what we’d tell any Bronx homeowner: don’t ignore it and don’t panic. You still have time and you still have options. What you do in the window between receiving that notice and an actual foreclosure filing can make the difference between walking away with money in your pocket or losing everything to a courthouse auction.

Your options at this stage generally include catching up on the missed payments if you have the ability, working out a loan modification with your lender, selling the property on the open market if there’s equity, or selling to a cash buyer quickly enough to pay off the mortgage and put remaining equity in your hands. 718Homebuyers can typically make an offer and close within 10 days — which in pre-foreclosure timing is significant breathing room. We’ve helped Bronx families at exactly this crossroads turn a crisis into a clean exit.

Can I sell my house in the Bronx if it’s already in foreclosure?

Yes — and this surprises a lot of homeowners who assume foreclosure means they’ve already lost the right to sell. Until a foreclosure sale is actually completed and title transfers to a new owner, you retain ownership of your property and the legal right to sell it.

This is true even after a judgment of foreclosure has been entered against you. As long as the auction hasn’t happened and the deed hasn’t changed hands, you can sell. We’ve closed deals in the Bronx with auction dates as close as two weeks out. It’s not comfortable, but it’s possible.

What selling during foreclosure accomplishes is simple: if your home is worth more than what you owe your lender — including all the accumulated fees, interest, and court costs — a sale pays off the mortgage debt, stops the foreclosure, and puts whatever equity remains in your pocket. That’s real money that would otherwise disappear into the auction process.

The catch is that at the later stages of foreclosure, a traditional sale through a real estate agent with a 60-90 day closing timeline often isn’t fast enough. That’s where a cash buyer with a 10-day closing capability becomes the practical option rather than just a convenient one.

If you’re in active foreclosure and want to know whether your numbers work for a sale, call us. We’ll run the math with you honestly — and if it doesn’t make sense for you to sell to us, we’ll tell you that too.

What is a foreclosure auction in the Bronx and what happens to my equity if my home sells at auction?

A foreclosure auction — formally called a foreclosure sale — is the final stage of the foreclosure process where your home is sold to the highest bidder at a public auction administered by the Bronx County courthouse. At this point the lender’s goal is simply to recover what they’re owed. Your equity, your belongings, your timeline — none of that is a consideration in the auction process.

Here’s the hard truth about auctions that most homeowners don’t know until it’s too late: the auction is not designed to get you fair market value. Properties routinely sell below market at foreclosure auctions because the buyer pool is limited to people with cash in hand that day, the property can’t be properly inspected beforehand, and there’s no negotiation. Institutional investors and professional auction buyers know this and price their bids accordingly.

If there’s equity in your home above what’s owed — meaning the auction sale price exceeds your total debt including fees — you are entitled to that surplus. But getting it isn’t automatic. You have to file a claim with the court, and many homeowners don’t know to do this or miss the window to file.

The far better outcome for any Bronx homeowner with equity is to sell before the auction ever happens. 718Homebuyers exists in large part for exactly this situation — to give families a real alternative to watching their equity get consumed by a process that was never designed to protect them. If you have an auction date on the calendar, call us before that date becomes your deadline.

Recent Bronx data shows auction sales typically close at 65% to 75% of fair market value, and under New York law, homeowners must file a “Notice of Claim to Surplus Monies” with the court within the statutory window before the deadline passes or those funds are paid out to other lienholders.

Source: NYS Courts — Surplus Monies Filing Instructions.

What is the difference between a short sale and selling to a cash buyer like 718Homebuyers?

Both are ways to sell a home that has a mortgage problem, but they work very differently and produce very different outcomes for the homeowner.

A short sale happens when your home is worth less than what you owe the lender and you ask the lender to accept less than the full payoff amount. The lender has to approve the sale price, which means you need their cooperation, and that approval process routinely takes three to six months. There’s no guarantee they say yes. If they approve it, your credit still takes a significant hit and depending on how it’s structured, you could still owe the difference — called a deficiency — depending on New York State law at the time.

Selling to us is a completely different transaction. We’re buying your home outright with cash. We don’t need lender approval, we don’t need bank financing, and we don’t answer to anyone but you in the transaction. If there’s enough equity to cover your mortgage payoff, we pay it off at closing and you walk away with the remainder. The whole process from offer to closing typically takes 10 days.

Short sales make sense in specific situations — particularly when you’re significantly underwater and need lender cooperation to avoid a deficiency judgment. Cash sales make sense when speed matters, when the property has equity, or when the condition of the home makes a traditional listing unrealistic. We’ll tell you honestly which situation you’re in when you call us.

Deficiency outcomes can be case-specific in New York and depend on the property, the judgment, and lender strategy. In any short sale, you should push for a written deficiency waiver as a condition of approval.

Source: NYS Senate — RPAPL § 1371.

I’m behind on my mortgage but I have equity in my Bronx home. What are my real options?

Having equity changes everything. It means you’re not trapped — you have choices, and the goal is to make sure you exercise those choices before the foreclosure process erodes them.

If you’re behind but still have significant equity — meaning your home is worth meaningfully more than what you owe including all back payments, interest, and fees — here are your realistic options in plain language.

You can catch up on the arrears if you have access to funds or can negotiate a repayment plan with your lender. You can apply for a loan modification to restructure what you owe going forward. You can list the home traditionally with a real estate agent if you have enough time before a foreclosure filing — though in New York’s market a traditional sale takes 60-90 days minimum. Or you can sell to a cash buyer quickly, pay off everything owed, and walk away with your equity intact rather than watching it disappear into court costs, attorney fees, and auction discounts.

718Homebuyers has helped Bronx families in exactly this situation walk away with tens of thousands of dollars they didn’t know they were going to be able to keep. The equity was always there — the question was whether they had enough time and the right option to capture it. That’s the conversation we want to have with you before it’s too late to have it.

HPD Violations & Code Enforcement

What are HPD violations and why are they a problem for Bronx homeowners trying to sell?

HPD stands for the New York City Department of Housing Preservation and Development. When your property doesn’t meet the city’s housing maintenance code — whether that’s a heat issue, a structural problem, lead paint, mold, pests, or any number of other conditions — HPD can issue violations against your property. Those violations become part of your property’s public record, attached to your address in the city’s database, visible to any buyer, any title company, and any lender who looks.

That visibility is exactly why HPD violations create problems when you try to sell. Traditional buyers using bank financing almost always hit a wall — lenders won’t approve mortgages on properties with open Class C violations, which are the most serious category. Even Class B violations can complicate or kill a conventional sale. And the longer violations sit open, the more they compound. The city can issue daily fees, escalate the violation class, and in serious cases initiate emergency repair work and bill the cost back to you as a lien against the property.

718Homebuyers works with HPD violation properties every single day — it’s one of our core specialties and frankly one of the situations where we provide the most value to Bronx families. We buy as-is, we don’t need bank financing, and we’re not scared off by a violation history that would send a traditional buyer running for the exit. If HPD violations have been standing between you and a sale, that stops being an obstacle the moment you call us.

As of early 2026, the Bronx continues to lead the city in violation density, with recent data showing that approximately 31% of privately-owned rental units in the borough carry at least one serious housing code violation. Fines have also scaled; Class B violations now carry penalties of up to $100 plus $10 per day, while Class C penalties can reach $1,250 per day for repeat heat and hot water offenses.

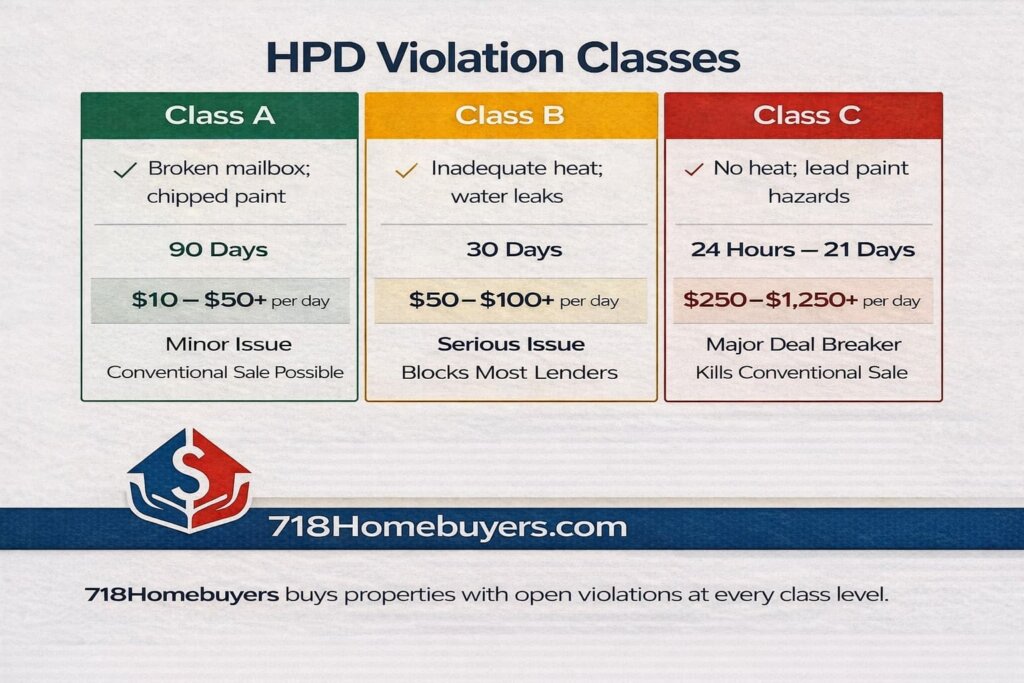

What is the difference between a Class A, Class B, and Class C HPD violation?

HPD categorizes violations into three classes based on how serious and how urgent the condition is. Understanding the difference matters because it affects your timeline, your financial exposure, and your options.

Class A violations are non-hazardous. These are maintenance issues that don’t pose an immediate threat — things like a broken mailbox, a missing light fixture in a common area, or minor painting issues. You’re given 90 days to correct them. The financial exposure is relatively low but they still show up on your record and need to be addressed.

Class B violations are hazardous. These represent conditions that are dangerous but not immediately life-threatening — things like inadequate heat, water leaks, pest infestations, or broken locks on building entry doors. You’re given 30 days to correct these. Fines are higher and lenders take them seriously.

Class C violations are immediately hazardous. This is the serious category — lead paint conditions, no heat in winter, structural dangers, severe mold, or vermin infestations at a level that threatens health and safety. These require correction within 24 hours to 21 days depending on the specific condition. Class C violations can trigger emergency HPD intervention, meaning the city does the repair work and sends you the bill as a lien. They will absolutely kill a conventional sale.

If your property has Class C violations and you’ve been struggling to figure out what to do with it, you’re not alone. 718Homebuyers has seen violation stacks that would make most buyers walk away on the spot. We don’t walk away — we’ve been solving exactly these situations for Bronx property owners since 2013 and we know how to move decisively when others hesitate.

Under 2026 regulations, Class A violations remain on a 90-day correction window, Class B on a 30-day window, and Class C violations typically require 24-hour remediation for heat/hot water, 14 days for self-closing doors, or 21 days for lead paint and window guards. Current fine schedules range from $10–$50 per day for Class A to $150–$1,200 per day plus specific “per-unit” surcharges for unresolved Class C hazards.

Can I sell my Bronx home with open HPD violations?

Yes — but your buyer pool shrinks dramatically the moment a traditional lender sees open violations on the record, particularly Class B or Class C. That’s the honest answer most people don’t get upfront.

Here’s what actually happens in a traditional sale when violations are present. The buyer’s attorney does a title search. The violations show up. The buyer’s lender either refuses to issue a mortgage commitment or requires the violations to be cleared as a condition of closing. Now you’re either paying out of pocket to remediate before you’ve even received your sale proceeds, or the deal falls apart entirely.

Selling to a cash buyer eliminates that problem entirely. We don’t use bank financing. There’s no lender looking over our shoulder, no mortgage commitment contingency, and no requirement that violations be cleared before closing. We price the condition of the property into our offer and we handle what needs to be handled after we close. That’s the transaction structure that actually works for a violation-heavy property.

One thing we always do is give you a clear, honest picture of how the violations are affecting the offer price. We’re not going to pretend they don’t exist or low-ball you without explanation. You deserve to understand exactly how we arrived at the number we’re offering so you can make an informed decision.

HPD did emergency repair work on my property and now I have a lien. What does that mean for selling?

When HPD violations go unaddressed — particularly Class C immediately hazardous conditions — the city has the authority to send its own contractors in to do the repair work and then charge the cost back to you. That charge becomes an Emergency Repair lien on your property, recorded against the deed, and it has to be satisfied before or at the closing of any sale.

The lien doesn’t prevent you from selling. What it does is reduce your net proceeds. At closing, the lien gets paid off from the sale proceeds just like a mortgage payoff would be. If the lien plus your mortgage payoff is less than your sale price, you still walk away with money. If the liens and mortgage together exceed what the property is worth, you’re in a more complicated situation that requires a deeper conversation.

Emergency Repair liens also accrue interest, which means the longer they sit the more they cost you. We’ve seen Bronx properties with multiple stacked emergency repair liens going back years — each one growing. The answer in most of those situations is still to sell, but the urgency is real because every month of delay costs money.

We handle lien payoffs at closing routinely. It’s not an unusual or complicated situation for us — it’s just part of the math we work through with you when we make an offer.

As of 2026, Emergency Repair Program (ERP) liens accrue interest at a rate of 7% per year, and while Bronx averages vary widely based on the scope of work, individual liens for boiler replacements or structural stabilization often range from $15,000 to over $45,000 per intervention.

I have a vacate order on my Bronx property. Can I still sell it?

A vacate order — issued by HPD or the Department of Buildings when a property is deemed unsafe for occupancy — is one of the more serious situations a property owner can face. It means the city has determined the building conditions are dangerous enough that no one should be living there. If tenants are present, they typically get relocated and you can face additional penalties and costs related to that displacement.

But a vacate order does not mean you’ve lost the right to sell your property. You still own it. You can still transfer title. What you cannot do is have anyone occupying it legally until the conditions that triggered the vacate order are remediated and the order is lifted.

For a traditional sale this is essentially a dead end — no conventional buyer is financing a vacated building and no tenant-occupied building with a vacate order is going to pass any standard inspection. For a cash buyer who specializes in distressed properties, it’s a different conversation entirely.

718Homebuyers has purchased vacated properties in the Bronx. We understand the DOB and HPD remediation process, we know what it costs to bring these buildings back, and we price accordingly. If you’re sitting on a vacated property and you’re not sure what your options are, the answer isn’t to let it sit and accumulate more violations and more liability. Call 718Homebuyers and let’s look at the numbers together — a vacate order is a serious situation but it’s not one you have to navigate alone.

Recent data through February 2026 shows hundreds of active vacate orders across the Bronx, frequently triggered by structural compromise or illegal conversions; lifting an order currently requires a certified professional to file for a “rescission” and can take 3 to 6 months to process through DOB/HPD inspections.

My Bronx property has lead paint violations. How serious is this and what are my options?

Lead paint violations are among the most serious HPD issues a property owner can face, and New York City has some of the strictest lead paint laws in the country. If your property was built before 1960 — and a significant percentage of Bronx housing stock was — and a child under six lives or has lived there, you’re in a high-scrutiny category under Local Law 1, the city’s primary lead paint statute.

The consequences of unaddressed lead paint violations are significant. HPD can issue Class C immediately hazardous violations requiring correction within 21 days. If you don’t comply, the city can conduct emergency lead abatement and bill you for it. There’s also civil liability exposure if a child in the property has been harmed — that’s a separate legal issue that goes beyond the violation itself.

Selling a property with open lead paint violations through traditional channels is extremely difficult. Buyers with children won’t touch it. Lenders financing buyers with children won’t approve it. Even buyers without children often walk away from the liability and the remediation cost.

718Homebuyers buys lead paint violation properties. We have experience with the remediation process, we understand the scope and cost, and we factor it into our offer rather than using it as a reason to walk away from the table. If you’re a Bronx property owner carrying lead paint violations and you’ve been stuck not knowing what to do, call 718Homebuyers — that’s exactly the conversation we’re built to have.

As of 2026, the Bronx continues to record the city’s highest rate of lead violations at approximately 73 per 1,000 units, while current NYC Local Law 1 mandates full abatement of friction surfaces upon turnover; professional remediation costs now average between $10,000 and $25,000 for a typical 1,200 sq. ft. unit.

How do I find out how many HPD violations are on my Bronx property?

This is public information and it’s easier to look up than most homeowners realize. The New York City Housing Information Portal — available at hpdonline.hpdnyc.org — lets you search any property by address and see its full violation history, open violations, complaint history, and any emergency repair charges on record.

What you’ll see when you search is every violation ever issued, whether it’s been certified as corrected or is still open, what class it is, and what the original condition was. It’s the same database that buyers, attorneys, and lenders look at when they’re evaluating your property.

If you pull your property record and the list is longer than you expected — or if you see open Class C violations you weren’t aware of — don’t let that be paralyzing. We’ve seen violation histories with dozens of open items across multiple classes. The length of the list doesn’t change the fundamental question, which is: what are your options given where things stand today? That’s a question we can help you answer honestly.

The HPD Online portal (hpdonline.hpdnyc.org) remains the primary public gateway as of 2026, featuring a recently modernized interface that now provides real-time updates on violation certifications and direct links to the HPD Enforcement Desk for document submissions.

Probate & Inherited Properties

What is probate and why does it affect my ability to sell an inherited Bronx property?

Probate is the legal process through which a deceased person’s estate is settled — debts get paid, assets get distributed, and ownership of property gets formally transferred to the rightful heirs. In New York State, probate is handled through the Surrogate’s Court, and in the Bronx that means the Bronx County Surrogate’s Court on Grand Concourse.

The reason probate affects your ability to sell is straightforward: until the court officially recognizes you as the legal owner or authorizes you to act on behalf of the estate, you don’t have the legal authority to sign a deed and transfer title. A title company won’t insure the sale, a buyer’s attorney won’t let their client close, and the transaction simply cannot happen.

This surprises a lot of families who assumed that because their parent or grandparent always said “this house goes to you,” the house just goes to them. Intent and legal ownership are two different things, and the gap between them is filled by the probate process.

The length and complexity of probate in New York varies significantly depending on whether there was a valid will, how many heirs are involved, whether anyone contests the will, and how organized the deceased’s affairs were. Simple estates with a clean will and cooperative heirs can move through in a few months. Contested or complex estates can take years.

We work with families at every stage of probate — some who haven’t even filed yet and some who are fully through the process and just ready to sell. Wherever you are in that timeline, we can help you understand your options.

As of early 2026, the average uncontested probate in Bronx County Surrogate’s Court takes 6 to 9 months, though 2025 procedural updates and increased staffing have aimed to resolve a backlog that previously pushed many cases beyond the 12-month mark.

What happens to a Bronx property if the owner dies without a will?

Dying without a will is called dying intestate, and it triggers a specific set of rules under New York State law that determines who inherits what. The property doesn’t just automatically pass to whoever was closest to the deceased — it passes according to a fixed legal hierarchy that doesn’t account for family dynamics, promises made, or who actually lived in or cared for the property.

In New York, if you die intestate with a spouse and children, the spouse gets the first $50,000 plus half the remainder, and the children split the other half. If there’s no spouse, the children split everything equally. If there are no children, it goes to parents, then siblings, then more distant relatives. The court works down the family tree until it finds living heirs.

For a Bronx property this creates real complications. You might end up with four, five, or six heirs who all have a legal ownership interest in a house — some of whom want to sell, some of whom don’t, some of whom haven’t spoken in years, and some of whom you may not even know exist. Every one of them has to agree or the court has to intervene.

We’ve navigated multi-heir situations many times. We understand that these aren’t just legal transactions — they’re family situations with history, emotion, and sometimes real conflict underneath them. We move at the pace the family needs and we work with whatever combination of heirs and attorneys is involved.

Under EPTL § 4-1.1, the 2026 New York intestate rules remain firm: the surviving spouse receives the initial $50,000 and one-half of the residue, with the remaining balance distributed to the children by representation.

I inherited a Bronx property with multiple heirs and not everyone agrees on selling. What can we do?

This is one of the most common and most emotionally difficult situations we encounter. One sibling wants to sell, another wants to keep the property, a third lives out of state and just wants the whole thing resolved. Meanwhile the property is sitting, taxes are accruing, maintenance isn’t getting done, and the disagreement is straining relationships that were already complicated by grief.

The hard legal reality is that no single heir can force a sale unilaterally — but they can force a partition action. A partition lawsuit asks the court to either physically divide the property among the heirs (which is rarely practical for a single-family home) or order it sold and the proceeds divided. Courts almost always order the sale in residential property cases.

The partition process works, but it’s slow, expensive, and adversarial. Attorney fees come out of the sale proceeds, the family relationship often doesn’t survive it, and the court-ordered sale process doesn’t optimize for getting you the best price.

The better outcome in almost every multi-heir disagreement we’ve seen is a direct conversation — sometimes with us facilitating — where everyone gets clear on what the property is actually worth, what each person’s share would look like, and what it would cost everyone in time, money, and family capital to let it drag into litigation. When people see those numbers side by side, the path forward usually becomes clearer.

We’re patient. We’ve worked through these situations before and we know how to move at the speed of family consensus rather than pushing anyone into a decision they’re not ready to make.

Under the Uniform Partition of Heirs Property Act (UPHPA) active in New York in 2026, the partition process typically takes 12 to 18 months to reach a resolution, with legal costs often ranging from $15,000 to $35,000 depending on the complexity of the title and heir disputes.

What is an estate sale and how is it different from a regular home sale in New York?

In real estate terms, an estate sale refers to the sale of a property that is part of a deceased person’s estate — it’s not the same as an estate sale of personal belongings, which is a different thing entirely. The distinction matters because an estate property sale has legal requirements that a standard sale between living owners doesn’t have.

The most important difference is authorization. In a regular sale, the owner signs the contract and the deed. In an estate sale, the person signing is either the executor named in the will or the administrator appointed by the court if there was no will. That person has a legal fiduciary duty to the estate and all its heirs — meaning they’re required to act in the best financial interest of everyone involved, not just themselves.

This fiduciary obligation means the executor or administrator typically can’t just accept whatever offer comes in first. They need to be able to demonstrate they acted reasonably on behalf of the estate. Working with a cash buyer who provides a clear, documented offer with a transparent valuation process actually supports that fiduciary obligation — it creates a paper trail that shows due diligence.

We work directly with executors and estate attorneys regularly. We understand the documentation they need, the timeline constraints they’re working under, and the fact that they’re often managing a sale while simultaneously managing grief and family dynamics. We make that process as straightforward as possible.

The inherited Bronx property I need to sell has been vacant for years and is in bad shape. Does that affect my options?

It affects your options with traditional buyers significantly. It doesn’t affect your options with us.

Vacant properties deteriorate faster than occupied ones — no one is catching the small leak before it becomes a big one, no one is keeping up with maintenance, and in some Bronx neighborhoods a visibly vacant property attracts additional problems over time. By the time a family is ready to deal with an inherited property that’s been sitting for two, three, or five years, the condition is often genuinely rough.

Traditional buyers using bank financing need the property to meet minimum habitability standards for their lender to approve a mortgage. A vacant property with years of deferred maintenance, potential mold, structural issues, or code violations almost never clears that bar without significant investment upfront — investment that heirs who live out of state or are managing their own financial situations often can’t or don’t want to make.

We buy properties in exactly this condition. We’ve walked through inherited Bronx homes that hadn’t been touched in a decade. The condition affects the offer price honestly and transparently — we’ll explain exactly what we’re seeing and how it factors into our number — but it doesn’t affect our willingness to buy. We’re in the business of solving these situations, not avoiding them.

What taxes do I owe when I sell an inherited property in New York?

This is a question where we’ll always encourage you to talk to a tax professional about your specific situation, because the answer depends on factors unique to you. But we can give you the framework that every heir selling an inherited Bronx property should understand.

The most important concept is stepped-up basis. When you inherit a property, your cost basis for tax purposes is generally stepped up to the fair market value of the property on the date of the original owner’s death — not what they originally paid for it. This is significant because it dramatically reduces or in many cases eliminates capital gains tax on the sale, even if the property appreciated substantially during the original owner’s lifetime.

For example, if your grandmother bought her Bronx home in 1975 for $40,000 and it’s worth $450,000 today, her capital gains exposure on a lifetime sale would be enormous. But if you inherit it at today’s value and sell it shortly after for $450,000, your taxable gain may be close to zero because your basis was stepped up to $450,000 at the time of inheritance.

New York State also has its own estate tax with its own thresholds, separate from the federal estate tax. Whether the estate itself owes tax before assets are distributed to heirs depends on the total value of the estate.

Again — talk to a CPA or estate attorney about your specific numbers. But don’t let fear of taxes stop you from exploring a sale before you understand what you’d actually owe, because the answer is often much better than people expect.

For 2026, the federal estate tax exemption is approximately $14.3 million per individual, while the New York State estate tax cliff remains around $7.1 million; the “stepped-up basis” rule continues to apply to inherited residential properties under current federal tax code.

We inherited a Bronx property that still has a mortgage on it. What happens now?

Inheriting a mortgaged property is more common than people realize, and it’s more manageable than it initially sounds — but it does require prompt attention.

Federal law — specifically the Garn-St. Germain Act — protects heirs who inherit mortgaged properties. Lenders cannot invoke the due-on-sale clause, which would normally allow them to demand full repayment when a property transfers ownership, when the transfer happens as a result of the owner’s death to a relative who will occupy the property. This means if you inherit your parent’s home and plan to live there, the lender generally has to let you assume the mortgage.

If you don’t plan to live there and want to sell, the situation is different. The mortgage still has to be paid off at or before closing — it comes out of the sale proceeds just like any other payoff. If the property is worth more than the mortgage balance, the difference comes to the estate and then to the heirs. If the mortgage balance exceeds the property value, you’re in an underwater situation that requires a different strategy, potentially including a short sale negotiated with the lender.

The one thing heirs should not do is simply stop making mortgage payments while the estate is being sorted out. The mortgage doesn’t pause because the owner died. Missed payments become a foreclosure risk that compounds every other challenge the estate is already dealing with.

As of 2026, federal protections under the Garn-St. Germain Act remains the standard in New York, preventing lenders from accelerating mortgages upon death to a relative; however, heirs must still maintain monthly payments to avoid default and potential foreclosure actions.

Selling As-Is & Distressed Properties

What does selling a home as-is actually mean in New York?

Selling as-is means you’re transferring the property in its current condition without making repairs, renovations, or improvements before closing. You’re not hiding defects — New York State still requires sellers to disclose known material conditions through the Property Condition Disclosure Statement — but you’re making clear that the price reflects the current state of the property and you’re not negotiating repair credits or fix-it contingencies after inspection.

For a distressed property in the Bronx, as-is is often the only practical path forward. The cost and time required to bring a severely deteriorated property up to a condition that would satisfy a conventional buyer and their lender can be prohibitive — especially for homeowners who are already under financial stress, dealing with an estate, or simply don’t have the bandwidth to manage a renovation project while navigating everything else life is throwing at them.

At 718Homebuyers, as-is isn’t a warning flag — it’s our default. We make offers on properties the way they are today, not the way they could be after $80,000 in renovations. We’ve bought Bronx homes with collapsed ceilings, flooded basements, fire damage, and everything in between. The condition tells us what the project costs. It doesn’t tell us whether we’re interested.

What kinds of distressed properties does 718Homebuyers buy in the Bronx?

The short answer is most of them. But here’s the fuller picture so you know whether your specific situation fits.

We regularly purchase properties with major structural damage including foundation issues, roof failures, and compromised load-bearing elements. We buy fire-damaged and smoke-damaged properties at every level of severity. We buy homes with severe water damage, mold infestations, and environmental contamination issues. We buy properties with full HPD violation stacks, active foreclosure filings, unpaid tax liens, and mechanic’s liens. We buy tenant-occupied properties including situations with non-paying tenants and active housing court cases. We buy probate properties, inherited properties, and properties caught in estate disputes.

What we don’t do is pretend the condition doesn’t affect the price. It does, and we’ll always be transparent about how. What we also don’t do is use condition as a reason to walk away from a family that needs a solution. 718Homebuyers exists specifically because there’s a category of Bronx property that the traditional real estate market simply cannot serve — and those homeowners deserve options just as much as anyone else.

How does 718Homebuyers determine what to offer on a distressed Bronx property?

This is one of the most important questions to ask any cash buyer, and you should be skeptical of anyone who won’t answer it clearly. We will.

Our offer is built on three numbers. First, the after-repair value — what the property would be worth in fully renovated condition based on comparable sales in that specific Bronx neighborhood. Second, the estimated cost to get it from current condition to that value — materials, labor, carrying costs, permits, and a realistic contingency because renovation projects always have surprises. Third, our margin — we’re a business and we need to make a profit to stay in business and keep helping families.

The formula looks like this: After-Repair Value minus Renovation Costs minus Our Margin equals your offer. We work backward from what the property can realistically be worth, not forward from a number we’d like to pay.

What this means for you is that our offer reflects actual neighborhood data and actual renovation costs — not a lowball number generated by an algorithm that’s never been inside a Bronx home. 718Homebuyers has been doing this since 2013. We know what things cost in this market and we know what properties sell for block by block. That knowledge is what makes our offers fair even when the property is in rough shape.

What repairs do I need to make before selling to 718Homebuyers?

None. That’s the point.

We’ve had homeowners apologize to us for the condition of a property before we’ve even walked in the door. Please don’t. The condition is our problem to solve after closing, not yours to fix before it. We factor everything we see into our offer so that you don’t have to spend money you may not have on repairs that may not even move the needle on a conventional sale.

You don’t need to clean it out either. If there are belongings, furniture, or decades of accumulated items in the property, leave them or take what you want — we handle the rest. We’ve cleared out full houses after closing so that heirs dealing with an estate don’t have to make that emotionally exhausting trip to the Bronx from wherever they’ve moved.

The only thing we need from you is an honest conversation about what you know about the property’s condition and history. Not a contractor’s report, not an inspection — just what you know. That conversation, combined with our own walkthrough, is everything we need to put a fair number on the table.

How is selling to 718Homebuyers different from listing with a real estate agent?

They’re genuinely different transactions designed for different situations, and the honest answer is that one isn’t always better than the other — it depends entirely on your circumstances.

A traditional listing with a real estate agent makes the most sense when your property is in good condition, you have time to wait 60 to 90 days for a conventional sale, you can handle the carrying costs during that period, and maximizing gross sale price is your primary goal. In that situation, the open market with a good agent will likely get you more money than we will.

Selling to 718Homebuyers makes the most sense when time is a factor — foreclosure, probate deadlines, financial pressure. When condition is a factor — the property won’t survive a traditional buyer’s inspection or lender appraisal. When simplicity is a factor — no showings, no contingencies, no deals falling through at the last minute because a buyer’s financing collapsed. When certainty is a factor — we close when we say we’re going to close.

The other thing a traditional listing doesn’t include is agent commissions, which in New York typically run five to six percent of the sale price, plus closing costs. We cover closing costs and charge zero commissions. So the gap between our offer and a traditional listing price is often smaller in net terms than it looks on paper.

We’ll always tell you honestly if we think a traditional listing is the better option for your situation. We’re solvers, not salespeople.

As of early 2026, the average real estate commission in New York City continues to hover between 5% and 6%, while the median “days on market” for Bronx residential properties has stabilized at approximately 63 days before reaching a signed contract.

What is a zombie property and how does 718Homebuyers help with them in the Bronx?

A zombie property is a home that has been abandoned — typically by an owner who left after receiving a foreclosure notice but before the foreclosure was actually completed. The owner assumed the bank would take over quickly. Instead the foreclosure stalled in New York’s slow court system, the bank never took title, and the property sat in legal limbo — nobody maintaining it, nobody responsible for it in any practical sense, deteriorating and often becoming a blight on the surrounding block.

New York State passed the Zombie Property Law in 2016 specifically to address this problem, requiring lenders to maintain vacant properties in foreclosure and empowering municipalities to enforce maintenance standards. But the law didn’t make zombie properties easy to sell — it just made them slightly less likely to completely collapse while the legal situation dragged on.

If you own a zombie property — or inherited one — in the Bronx, the situation feels overwhelming because it combines an unresolved foreclosure with a deteriorating physical asset and ongoing legal obligations. 718Homebuyers has navigated this exact combination. We understand the legal overlay, we know how to work with title companies on properties with complicated foreclosure histories, and we can move decisively when other buyers would simply walk away.

Recent Q1 2026 data indicates that approximately 3.3% of New York residential properties in foreclosure are “zombies,” and 2026 legislative updates to the Zombie Property Law have increased daily penalties for lenders failing to maintain these sites from $500 to $650 per day.

Can I sell my Bronx home if it has unpaid property taxes or tax liens?

Yes — and this is another situation where the fear of the problem is often worse than the problem itself once you actually look at the numbers.

Unpaid property taxes in New York City become a lien against your property. If left long enough, the city can sell that lien to a third-party lien buyer, which adds interest and fees and starts a separate foreclosure clock running. New York City’s tax lien sale process has been a source of significant controversy and ongoing legislative attention because of the disproportionate impact on long-term homeowners in neighborhoods like the Bronx who fall behind during financial hardship.

Like a mortgage payoff or an HPD emergency repair lien, unpaid tax liens get satisfied at closing from your sale proceeds. They don’t prevent a sale — they just reduce your net. 718Homebuyers handles lien payoffs as a routine part of every transaction. We coordinate with the title company to identify every lien on the property, calculate the total payoff amounts, and structure the closing so everything gets resolved in one transaction.

If you’re not sure what liens are on your Bronx property, we can help you find out. A title search will surface everything, and we run one as part of our standard process before making a final offer.

In 2026, NYC moved away from the traditional private tax lien sale model toward a more publicly controlled approach, and the rules have been evolving fast.

Source: NYC Council Legislation — Intro 1407-2025

The Cash Buying Process

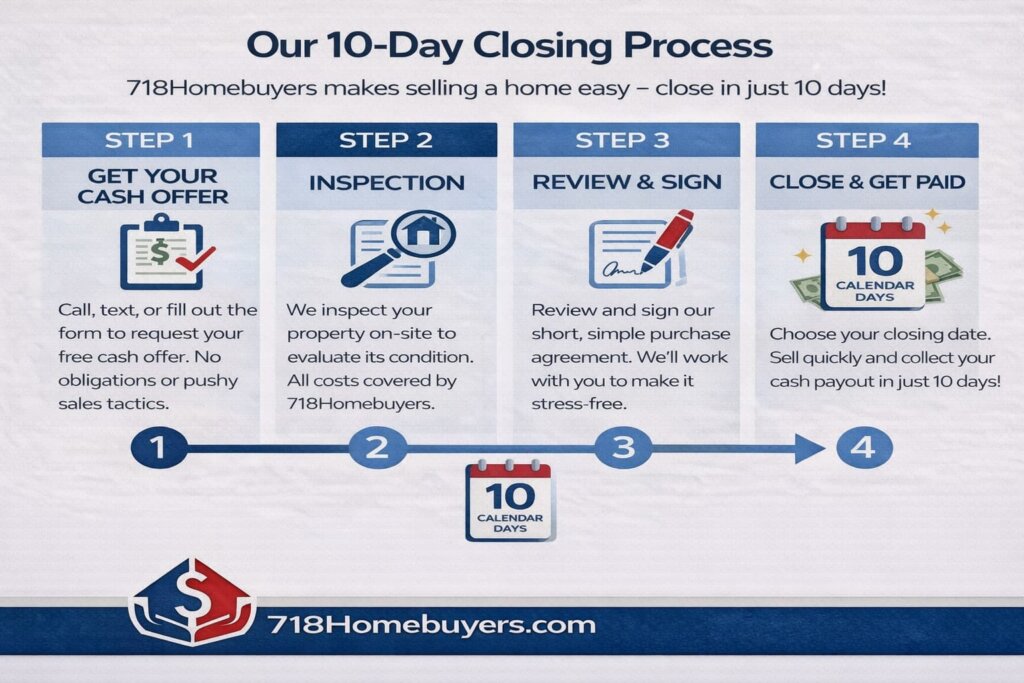

How does the 718Homebuyers cash buying process actually work from start to finish?

Most homeowners who call us have never sold to a cash buyer before and aren’t sure what to expect. The process is simpler than a traditional sale in almost every way, and we’ve designed it specifically to reduce the burden on you rather than add to it.

It starts with a phone call or form submission through 718homebuyers.com. We ask some basic questions about the property — address, general condition, your situation, your timeline. No judgment, no pressure. We’re just gathering enough information to know whether we can help and to prepare for the next step.

From there we schedule a walkthrough. We come to the property, we look at everything honestly, and we ask questions. This isn’t an interrogation — it’s us doing our homework so we can make you a real offer, not a placeholder number that changes later. The walkthrough typically takes 30 to 60 minutes depending on the size and condition of the property.

Within 24 hours of the walkthrough we present you with a written cash offer. We walk you through how we arrived at the number so there are no mysteries. You take whatever time you need to consider it — we don’t use countdown timers or high-pressure tactics because that’s not who we are.

If you accept, we open title, your attorney reviews everything, and we move toward closing. For straightforward transactions 718Homebuyers can close in as few as 10 days. For more complex situations involving probate, lien resolution, or multiple heirs, we work on your timeline. At closing you receive your funds — typically by wire transfer or certified check — and the transaction is complete.

That’s it. No showings, no open houses, no financing contingencies, no last-minute surprises.

Is a cash offer from 718Homebuyers a guaranteed offer or can it change?

This is a fair and important question and you deserve a straight answer.

Our initial offer after a walkthrough is based on everything we can see and verify at that point. In the vast majority of our transactions that number holds through closing. We don’t use the tactic of making an attractive offer upfront and then re-trading the price after you’ve emotionally committed to selling — that practice exists in this industry and it’s something we explicitly reject.

The situations where a number can change are limited and specific. If a title search reveals liens or encumbrances we weren’t aware of that materially change the financial picture, we’ll have an honest conversation about it. If conditions inside the property are significantly different from what was visible during the walkthrough — a structural issue that wasn’t accessible, for example — we’ll discuss it. We’ll always explain exactly what changed and why, and you always retain the right to walk away with no obligation.

What we commit to is transparency at every step. 718Homebuyers has been operating in the Bronx since 2013 and our reputation is built on families who trusted us and got exactly what we promised. We don’t have a business without that trust and we don’t take it lightly.

How fast can 718Homebuyers really close on a Bronx property?

Ten days is our standard for a straightforward transaction — meaning clear title, no complex lien situations, no probate involvement, and a cooperative seller who’s ready to move. We’ve hit that timeline consistently because we use cash, which eliminates the mortgage underwriting process that causes most conventional closings to take 45 to 60 days.

Here’s what happens in those 10 days. Day one through three: we open title with our title company and they begin the title search. Days three through seven: title search completes, any issues get identified and addressed, closing documents get prepared. Days eight through ten: closing is scheduled, documents are signed, funds are transferred.

For more complex transactions the timeline extends but never without reason. A probate sale might take 30 to 60 days because we’re waiting on court authorization rather than anything on our end. A property with multiple liens might take a few extra days to coordinate all the payoffs. A multi-heir situation moves at the pace of family consensus. In every case 718Homebuyers is ready to close the moment the legal and logistical pieces are in place — we’re never the bottleneck.

If you have a specific deadline — an auction date, a court date, a financial deadline — tell us upfront. We’ll tell you honestly whether we can hit it.

Do I need a real estate attorney to sell to 718Homebuyers?

In New York State, real estate closings are attorney-supervised transactions — unlike many other states where title companies handle closings without attorneys. That means yes, you should have your own attorney representing your interests at closing. We have ours. You should have yours.

If you don’t have a real estate attorney, we can refer you to attorneys who have worked on transactions with us before and who understand the Bronx market. We want to be clear though — these are independent attorneys who represent you, not us. Their job is to make sure your interests are protected in the transaction, which is exactly how it should work.

Attorney fees for a straightforward cash sale closing in New York are typically modest compared to the overall transaction. 718Homebuyers covers standard closing costs as part of our offer — your attorney fee is separate and yours to pay, but it’s a manageable number that shouldn’t be a barrier to moving forward.

As of early 2026, typical real estate attorney fees for a residential cash sale closing in the Bronx generally range from $1,500 to $3,000, depending on the complexity of the title and the volume of liens requiring resolution.

What documents do I need to sell my Bronx home to 718Homebuyers?

Less than you probably think, and we help you gather what’s needed rather than leaving you to figure it out alone.

The core documents for any residential sale in New York include proof of identity, the deed to the property, and any mortgage statements showing current payoff amounts. If there are known liens — tax liens, HPD emergency repair charges, mechanic’s liens — any documentation you have on those is helpful but not required since the title search will surface them anyway.

For estate and probate sales, we’ll need documentation of your legal authority to act on behalf of the estate — typically Letters Testamentary if you’re an executor named in a will, or Letters of Administration if you were appointed by the court in an intestate situation. Your estate attorney will have these documents.

For properties with active foreclosure filings, any notices or legal documents you’ve received from the lender or the court are helpful context, though again our title search will pull the public record.

If you’re not sure what you have or where to find it, call us before you spend time digging through paperwork. We’ll tell you exactly what we need for your specific situation and nothing more. 718Homebuyers has guided hundreds of Bronx homeowners through this document process — it’s never as complicated as it feels at the start.

Will 718Homebuyers lowball me because my property is distressed?

We understand why people ask this and we don’t take offense at it. The cash buyer industry has a reputation problem in some markets because there are operators who do exactly that — make an artificially high number to get you emotionally committed, then slash the price right before closing when you feel like you have no other options.

That is not how 718Homebuyers operates and it never has been.

Our offer reflects the actual market math — after repair value minus realistic renovation costs minus a fair margin for our risk and profit. The distressed condition of the property affects the offer price because it genuinely affects the cost and risk of the project. But the margin we apply is consistent and reasonable, not inflated because we think you’re desperate.

The best protection you have is to understand how we arrived at our number. Ask us. We’ll walk you through every component of the offer. If you want to get a second opinion from another cash buyer, do it — we’d rather you feel completely confident in the decision you’re making than feel pressured into something you’re uncertain about. A homeowner who understands and trusts the offer is a better closing than one who accepted reluctantly and regrets it.

We’ve been in the Bronx since 2013 and we intend to be here for another decade. Our business runs on referrals from families we’ve helped. That only works if we treat people right.

What happens to my personal belongings when I sell to 718Homebuyers?

You take what you want and leave the rest — it’s genuinely that simple.

We don’t require you to do a full cleanout before closing. We don’t charge you for items left behind. We understand that for a lot of the situations we work in — estate sales, foreclosures, properties that have been vacant for years — a full cleanout is either logistically impossible, emotionally overwhelming, or both.

Take the things that matter to you. Family photos, heirlooms, documents, whatever has personal or financial value. Leave everything else. We handle the cleanout after closing as part of our renovation and rehab process.

For families dealing with an inherited property where a parent or grandparent lived for decades, this is often one of the most meaningful parts of working with 718Homebuyers. You don’t have to rent a dumpster, organize a cleanout crew, or make a dozen trips to the Bronx to clear out a lifetime of belongings before you’re allowed to close. You get to focus on what actually matters.

Tenant-Occupied Properties

Can I sell my Bronx rental property if it still has tenants living in it?

Yes — and this is one of the most misunderstood situations in New York real estate. Owning a tenant-occupied property does not strip you of your right to sell it. What it does is add a layer of legal complexity that affects who can buy it and how the transaction gets structured.

The complexity comes from New York’s tenant protection laws, which are among the strongest in the country. Tenants in the Bronx have significant rights that survive a sale — meaning the new owner takes the property subject to whatever lease or tenancy arrangement was in place when they bought it. You cannot evict tenants simply because you want to sell, and a sale does not automatically terminate a tenancy.

For traditional buyers using bank financing, tenant-occupied properties create real obstacles. Lenders financing owner-occupants won’t approve a mortgage on a property where the buyer can’t legally take possession. Investors financing through conventional channels face their own set of underwriting restrictions on occupied properties with complicated tenancy histories.

718Homebuyers buys tenant-occupied properties regularly. We understand New York’s rent stabilization laws, we know how to evaluate an existing tenancy situation, and we’re experienced at structuring transactions that work within the legal framework rather than trying to work around it. If you’re a Bronx landlord who needs to exit a rental property regardless of who’s living in it, that’s a conversation we’re built to have.

In 2026, rent-stabilized units comprise nearly 50% of the Bronx rental stock; while the 2019 Housing Stability and Tenant Protection Act remains the primary framework, 2025-2026 updates have further tightened “owner occupancy” eviction rules and increased the burden of proof for landlords seeking to recover units for personal use.

What are my rights as a landlord trying to sell a rent-stabilized property in the Bronx?

Rent stabilization is one of the defining features of the Bronx rental market and one of the most misunderstood by landlords trying to sell. Understanding your rights — and your limitations — before you try to sell is essential.

As a landlord you have the right to sell your rent-stabilized property at any time. The stabilization status of the units does not prevent a sale and does not require tenant consent. What it does is transfer to the new owner — whoever buys your building buys it with the rent-stabilized tenants in place, subject to all the same rules and restrictions you were operating under.

What you cannot do is use a pending sale as justification to remove rent-stabilized tenants. You cannot offer buyouts that are coercive or that misrepresent the tenant’s rights. You cannot refuse to renew leases simply because you’re planning to sell. New York’s 2019 Housing Stability and Tenant Protection Act significantly strengthened tenant protections and the penalties for landlord violations are real.

What this means practically for a sale is that your buyer pool is limited to investors who are comfortable owning and operating rent-stabilized units — which is a smaller pool than the general market but a real and active one. 718Homebuyers operates in exactly that pool. We evaluate rent-stabilized properties based on their actual income, their actual expenses, and the realistic trajectory of the tenancy situation — not on speculative scenarios that assume tenants will disappear.

Under 2026 regulations, all buyout offers must be accompanied by a formal “Tenant Disclosure Form” notifying the tenant of their right to remain; furthermore, the 2025 Mayoral transition has led to stricter enforcement of anti-harassment statutes regarding frequent or unsolicited buyout solicitations.

I have a non-paying tenant in my Bronx property. Does that make it impossible to sell?

It makes it harder to sell through traditional channels. It does not make it impossible to sell to 718Homebuyers.

A non-paying tenant is a landlord’s nightmare for reasons that go beyond the immediate lost rent. In New York City the eviction process is one of the longest and most tenant-protective in the country. Getting a non-paying tenant out through Housing Court involves filing a nonpayment petition, attending multiple court dates, obtaining a judgment of possession, and then waiting for a City Marshal to execute the warrant of eviction — a process that can take anywhere from several months to well over a year depending on court backlog and the tenant’s legal representation.

For a traditional buyer, an active non-paying tenant with an ongoing Housing Court case is a red flag that kills most deals before they start. The buyer’s lender won’t finance it, and most investors don’t want to inherit someone else’s eviction case.

We’ve purchased Bronx properties with active nonpayment proceedings, warranted evictions waiting on marshal scheduling, and tenants who hadn’t paid rent in over a year. We price the situation into our offer honestly — the carrying cost of the eviction timeline and the lost rent are real costs that affect the number — but we don’t use a difficult tenant situation as a reason to walk away from a landlord who needs out.

As of February 2026, Bronx Housing Court continues to face a significant bottleneck with average non-payment cases stretching 9 to 14 months from initial filing to marshal execution; recent data indicates nearly 40,000 active eviction filings currently pending in the Bronx alone.

What is cash for keys and is it something 718Homebuyers uses?

Cash for keys is a negotiated arrangement where a landlord or new property owner offers a tenant a cash payment in exchange for voluntarily vacating the property by a specific date — surrendering their keys and leaving the unit in acceptable condition. It’s not an eviction. It’s a voluntary agreement that benefits both parties when structured correctly.

For the tenant, it’s money in hand and a cleaner exit than a formal eviction proceeding that damages their rental history. For the property owner, it’s a faster and less expensive resolution than going through Housing Court — avoiding months of proceedings, attorney fees, and marshal costs.

Cash for keys is a legitimate tool that 718Homebuyers uses in appropriate situations. We’re transparent about it. It’s not coercive when done correctly — the tenant has the right to say no, continue their tenancy, and force the formal eviction process if that’s their preference. What it does is give both parties an opportunity to resolve the situation in a way that works better for everyone than an adversarial court process.

The amount offered in a cash for keys negotiation depends on the specific situation — how long the tenant has been there, what the local rental market looks like, how complicated the eviction case would be, and what a reasonable relocation amount represents given the circumstances. 718Homebuyers approaches these conversations with respect for the tenant’s situation while being clear about the options on the table.

Typical 2026 cash for keys offers in the Bronx range from $2,500 to $7,500 for market-rate units, though they must strictly avoid “self-help” tactics; NY law now classifies any interruption of essential services or changing of locks as a misdemeanor punishable by fines up to $10,000.

What happens to my tenants’ security deposits when I sell my Bronx rental property?

Security deposits are one of the details that landlords sometimes overlook in the urgency of a sale and one that can create real legal exposure if handled incorrectly.

In New York, security deposits belong to the tenant — not the landlord. You’re holding them in trust. When you sell the property, you are required to transfer all security deposits to the new owner, who then becomes responsible for them. This transfer needs to be documented, the tenant needs to be notified in writing within a specific timeframe, and the new owner’s name and address for future communications needs to be provided to each tenant.

If you fail to transfer security deposits properly, you can face personal liability to the tenants even after the sale closes. This is a detail that your real estate attorney handles at closing as part of the transaction documentation — but you should be aware of it going in so you have the deposits organized and accessible.

718Homebuyers walks through the security deposit situation as part of our standard due diligence on tenant-occupied properties. We identify every tenant, every deposit amount on record, and we make sure the transfer is handled correctly at closing so that neither you nor we are exposed to claims after the fact.

Under GOL § 7-108, landlords must transfer all security deposits to the new owner within five days of the property transfer and must notify tenants by registered or certified mail of the new owner’s contact information; failure to return or transfer deposits within the 14-day statutory window remains a strictly enforced penalty.

My Bronx tenants have a lease that doesn’t expire for another year. Can I still sell?

Yes — a lease that hasn’t expired does not prevent a sale. What it does is transfer to the new owner along with the property. The buyer steps into your shoes as landlord and is bound by the same lease terms you agreed to — the rent amount, the expiration date, the renewal terms, and any other provisions in the original lease agreement.

For a buyer who wants to occupy the property themselves this is a significant obstacle — they generally can’t take possession until the lease expires, and in New York breaking a residential lease to accommodate an owner’s personal use is extremely restricted under current law. That’s why active leases effectively eliminate owner-occupant buyers from your pool.

For an investor buyer — which is exactly the category 718Homebuyers falls into — an active lease with a paying tenant is not necessarily a negative. A tenant paying rent on time under a lease is actually a stable income stream, and we evaluate it as such. The question is whether the rent is at or near market rate and what the condition and history of the tenancy looks like.

If your tenant is paying, has been stable, and the lease terms are reasonable, the active lease may have less impact on our offer than you’d expect. Call 718Homebuyers and give us the full picture — we’ll evaluate it honestly and explain exactly how the lease factors into our number.

What is a preferential rent and how does it affect my ability to sell my Bronx rental property?

Preferential rent is a rent-stabilized concept that trips up a lot of Bronx landlords and has become significantly more complicated since the 2019 Housing Stability and Tenant Protection Act.

A preferential rent exists when a landlord charges a stabilized tenant less than the legal regulated rent they’re actually entitled to charge — often as an incentive to attract or retain a good tenant. The difference between what’s being charged and what could legally be charged is the preferential amount.

Before 2019, landlords could revert to the higher legal regulated rent upon lease renewal. The 2019 law changed that dramatically — now preferential rents are essentially locked in for the life of the tenancy. If your tenant has a preferential rent, they keep it as long as they stay. You can only raise it by the annual Rent Guidelines Board percentage applied to the preferential amount, not the legal regulated rent.

For a sale, this matters because a building with below-market preferential rents across multiple units has a lower actual income than its legal rent roll suggests — and investors value income-producing properties based on actual income, not theoretical maximums. 718Homebuyers accounts for preferential rents accurately when evaluating multi-unit Bronx properties. We look at what the building actually earns, not what it could theoretically earn in a scenario that current law no longer permits.

For leases commencing between October 1, 2025, and September 30, 2026, the NYC Rent Guidelines Board has set increases at 3% for one-year leases and 4.5% for two-year leases; these percentages must be applied to the preferential rent, which remains the permanent base for the duration of the tenancy.

Bronx Market & Legal Context

What makes the Bronx real estate market different from the rest of New York City?

The Bronx is not a discount version of Manhattan or Brooklyn. It’s a distinct market with its own dynamics, its own housing stock characteristics, its own community fabric, and its own economic trajectory — and understanding those differences is what separates a buyer who actually knows this borough from one who’s just running numbers on a spreadsheet.

The Bronx has the highest percentage of renter-occupied housing of any borough in New York City, which means the owner-occupied residential sale market is proportionally smaller and more relationship-driven than in other boroughs. When a Bronx homeowner sells, they’re often selling a property that has been in the family for decades — sometimes generations. These aren’t transactions, they’re transitions, and they require a level of care and local knowledge that out-of-borough investors frequently underestimate.

The housing stock is heavily concentrated in pre-war multifamily buildings and post-war co-ops, with pockets of single and two-family homes in neighborhoods like Pelham Bay, Throggs Neck, Riverdale, and Morris Park that represent the core of 718Homebuyers’ acquisition focus. These properties carry their own maintenance histories, their own violation patterns, and their own valuation logic that doesn’t translate directly from other markets.

The Bronx is also in the middle of a genuine and significant redevelopment wave — particularly in the South Bronx along the waterfront and in neighborhoods like Mott Haven and Port Morris — that is reshaping values, attracting institutional capital, and creating both opportunity and displacement pressure simultaneously. 718Homebuyers has watched this evolution from the ground since 2013 and understands where the market is going, not just where it’s been.

As of early 2026, the median home sale price in the Bronx has risen to approximately $650,000, reflecting a 2.4% year-over-year appreciation; meanwhile, major infrastructure projects like the $3 billion Metro-North Penn Station Access Project are driving new investment in the East Bronx.

What Bronx neighborhoods does 718Homebuyers serve and why does hyperlocal knowledge matter?

718Homebuyers serves all 25 zip codes across the Bronx — from Wakefield and Woodlawn in the north to Mott Haven and Hunts Point in the south, from Riverdale and Spuyten Duyvil in the west to Pelham Bay and City Island in the east. Every neighborhood. No exceptions.

But serving every zip code isn’t the same as knowing every zip code, and that distinction matters enormously when you’re trying to get a fair offer on your property. A cash buyer who covers all five boroughs from an office in Midtown Manhattan is working off regional comps and general assumptions. We’re working off block-level knowledge built over more than a decade of buying, renovating, and selling Bronx properties specifically.

That hyperlocal knowledge shows up in the offer. We know that two properties with identical square footage and similar condition can have meaningfully different values based on which side of a major thoroughfare they’re on, which school zone they fall in, what the transit access looks like, and what the immediate block’s trajectory has been over the past three years. Those nuances don’t show up in an algorithm. They show up in experience.

For a homeowner trying to evaluate whether an offer is fair, the question to ask any buyer is not just what they’re offering but why. At 718Homebuyers we can tell you exactly what comparable properties in your specific neighborhood have sold for, what the renovation costs look like in your area, and how we arrived at every component of our number. That transparency is only possible because we actually know this market.

In 2026, property values remain highly localized: Mott Haven averages around $769,000 with a 5.3% annual growth, while stable residential areas like Throggs Neck and Wakefield see median prices between $640,000 and $690,000.

What is the New York City transfer tax and how does it affect a Bronx home sale?

The New York City transfer tax is a tax imposed on the sale of real property in the five boroughs, paid at closing. For residential properties it’s calculated as a percentage of the sale price and it’s one of the closing costs that sellers need to understand before they can accurately calculate their net proceeds.

For residential properties selling for under $500,000 the NYC transfer tax rate is 1% of the sale price. For properties at $500,000 and above the rate increases to 1.425%. On top of the city tax, New York State imposes its own real estate transfer tax at 0.4% of the sale price — bringing the combined rate to either 1.4% or 1.825% depending on which threshold your property falls into.

There’s also the NYC Mansion Tax, which applies to residential sales at $1 million and above at a base rate of 1% with escalating rates for higher price points. Most Bronx residential transactions fall below the mansion tax threshold but it’s worth knowing exists.

At 718Homebuyers we cover standard closing costs as part of our offer — but transfer taxes in New York are typically a seller responsibility and factor into your net proceeds calculation. We walk every seller through a complete net proceeds estimate before they make a decision so there are no surprises at the closing table.

Current 2026 rates for residential sales remain at 1% for values under $500k and 1.425% above that mark for NYC, combined with the 0.4% NY State rate; the Mansion Tax continues to follow a graduated scale starting at 1% for sales of $1 million or more.

What is the New York City property tax system and how does it affect Bronx homeowners?

New York City’s property tax system is one of the most complex and frequently criticized in the country — and Bronx homeowners are disproportionately affected by its structural inequities in ways that aren’t always obvious until you’re trying to sell.

The city assesses properties at a fraction of their market value using a system that was established decades ago and has not kept pace with market realities. The result is a system where similar properties in different neighborhoods can carry wildly different effective tax rates, and where long-term homeowners in appreciating neighborhoods often face rapidly increasing tax bills that don’t reflect their actual income or ability to pay.

For a homeowner trying to sell, unpaid property taxes are the most immediate concern — as discussed in the tax liens section above, they become liens that must be satisfied at closing. But the broader context matters too: a Bronx property with a high property tax burden relative to its rental income is less attractive to investor buyers, which affects your market and can affect offer prices.

Understanding your current assessment, your tax bill, and whether you qualify for any of the available exemptions — Senior Citizen Homeowner Exemption, Disability Exemption, Veterans Exemption among others — is worth doing before you make any decisions about selling. 718Homebuyers can help you think through how your tax situation affects your net proceeds and your options.

As of the 2025/26 tax year, the Class 1 property tax rate is set at 19.843%, the lowest in a decade; current income thresholds for the Senior Citizen Homeowner Exemption (SCHE) and Disabled Homeowners’ Exemption (DHE) have been maintained to support residents earning $58,399 or less.

What is Article 78 and when does it matter for a Bronx property sale?

Article 78 of the New York Civil Practice Law and Rules is a legal proceeding used to challenge decisions made by government agencies — including decisions by the Department of Buildings, HPD, the Board of Standards and Appeals, and other city agencies that affect your property. It’s named for the article of the CPLR that governs it.